What Is Help to Buy?

Over recent years there have been a number of initiatives to help potential purchasers buy property in order to boost the housing market, for example, the First Time Buyer Stamp Duty Exemption initiative, which ran from 2010 to 2012. The current Help to Buy initiative has had a significant impact.

The Government’s Help to Buy scheme enables people to buy a home, priced up to £600,000.00, with a deposit as little as 5%. The scheme is not limited to first time buyers and existing home owners are also eligible for assistance under the scheme.

There are two options available under the Help to Buy scheme and a local new homes developer and/or mortgage advisor can help to advise which scheme is suitable for a purchaser:-

1. The Help to Buy: Equity Loan

The Equity Loan scheme is only available on new build homes and is available to first time purchasers as well as existing homeowners looking to move, provided that the property being acquired is a new build property with a purchase price of up to £600,000.00 in England, £400,000.00 in Scotland and £300,000.00 in Wales.

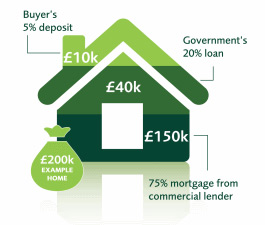

A 5% deposit is required, but with an Equity Loan, the Government will provide a 20% Equity Loan to help top up the deposit meaning that a 75% mortgage will be required by the purchaser.

The Equity Loan is separate from the mortgage and is entered into between the purchaser and the Government. The Equity Loan is interest free for the first 5 years; interest will be payable from year 6 and this should be taken into account when considering affordability. After the 5 year interest free period has ended, the borrower will be charged a fee of 1.75% of the loan’s value and this will increase every year at 1% above inflation.

The Equity Loan can be repaid at any time and if repaid within the first 5 years, no interest charges will be payable by the purchaser. Alternatively, the Equity Loan can be repaid when the property is sold or at the end of the mortgage period. When the Equity Loan is repaid, 20% of the sale price will be repayable, regardless of whether there has been an increase or decrease in the value of the property.

The below example delineates the typical breakdown for a home with a value of £200,000.00:-

There are limitations to the Equity Loan scheme as a purchaser will not be able to sublet the property or enter a part exchange deal on their existing home. In addition, the purchaser must not own any other property at the time that the new home is purchased with the assistance of an Equity Loan.

The Equity Loan scheme was launched in 2013 and recent statistics show that 33,911 properties have been acquired using the scheme up to 30th September 2014, 84% of which are first time buyers.

Due to the impact of the Equity Loan scheme, in March 2014, George Osborne announced that the scheme in England would be extended to 2020, in order to retain confidence in house building.

2. The Help to Buy: Mortgage Guarantee

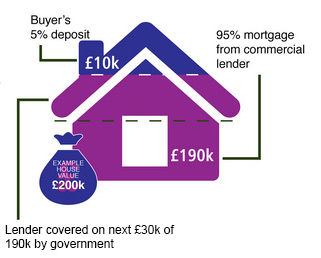

Over the last few years mortgage lenders have been requesting large deposits from purchasers, effectively pricing potential purchasers out of the market. In reality, many of these potential purchasers are able to afford the monthly mortgage payments, but struggle to raise a sufficient deposit to secure a mortgage. To assist, the Government introduced the Mortgage Guarantee scheme, which will run until the 31st December 2016, and enables lenders to offer homebuyers 80% to 95% mortgages.

With the Mortgage Guarantee scheme, the Government offers lenders the option to purchase a guarantee on the loans they supply (above the 80% loan to value ratio) in order to support them in providing 95% mortgages to purchasers as delineated in the below example:-

A mortgage under the Mortgage Guarantee scheme works like any other mortgage. The lender will ensure that the purchaser can afford the mortgage and that there is no history of payment difficulties.

To qualify for a mortgage supported by Help to Buy: Mortgage Guarantee:-

- The property could be an existing or new-build home in the UK, priced up to £600,000.00 in England, Scotland or Wales.

- The purchaser must not own any other property anywhere in the world at the time that they purchase the home supported by the Mortgage Guarantee scheme.

- The mortgage must be a repayment one, not interest only. Offset and guarantor mortgages are also excluded from the scheme.

- The property must not be sublet.

- The purchaser cannot use the Mortgage Guarantee scheme with any other Government scheme such as Help to Buy – Equity Loan or Shared Ownership. The deposit for the property cannot come from a Government scheme either.

- The purchaser does not have to pay any additional fee to the Government to get a Help to Buy supported mortgage,

- The size of the mortgage applied for must be less than 4.5 times of the purchaser’s income.

Under the Mortgage Guarantee scheme, once the property is sold, the owner would achieve 100% of the sale price.

Recent statistics show that 18,564 mortgages have been completed in the first 9 months of the scheme, with 79% being undertaken by first time buyers and the largest uptake being outside of London and the South East.

Gareth Richards, Conveyancing Association member and Legal Director of specialist conveyancing company Convey Law, commented as follows:

Will Help to Buy instigate a return to irresponsible lending?

“The Government’s stance is that various rules have been initiated to ensure that this is not the case. For example, no interest-only or offset mortgages are allowed under the schemes and the schemes cannot be used for the purchase of second homes or for buy to let investors. In addition, lenders are required to ensure borrowers are subject to stringent affordability checks, which are designed to combat a return to times of reckless lending.”

Will Help to Buy create another housing boom?

“Many commentators fear that Help to Buy will simply allow some relatively well-off people to move up the housing ladder.

“Critics, including the Labour Party, state that Help to Buy does nothing to address the shortage of affordable homes and would rather place more focus on house building. Treasury officials suggest that the scheme was designed to correct a failure in the market and stimulate builders to build again.

“The Bank of England is keeping a close eye on the second phase of Help to Buy, along with the housing market as a whole. Every three months a steering committee meets and can make recommendations to Government about extending or restraining the scheme.

“We believe that the Help to Buy schemes have helped to stimulate the housing industry and subsequently the economy as a whole. The schemes have provided much needed access to deposit funds to help first time buyers get onto the housing ladder. First time buyers start conveyancing chains and hence they stimulate the housing industry. Traditionally, once the housing market is in full swing – so is the greater UK economy.

“Help to Buy will not create another housing boom in isolation. Affordability of lending finance and responsible lending are the key to a buoyant and stable housing market with steady, healthy growth.”

Where can I obtain more information on Help to Buy?

For further information, please refer to www.helptobuy.org.uk.

February 13, 2015